Free D 422 North Carolina Form

Free D 422 North Carolina Form

Filling out the D 422 North Carolina form can be a daunting task, and many individuals inadvertently make mistakes that could lead to penalties or complications. One common mistake is failing to read the instructions thoroughly. Many people jump right into the form without understanding who should use it or the specific conditions that apply. This can lead to unnecessary penalties if the form is completed when it is not required.

Another frequent error involves miscalculating the required annual payment. Individuals often overlook the importance of accurately completing Part I, where they must determine their tax from the previous year. If they mistakenly enter the wrong figure or fail to account for tax credits, they may end up with an incorrect annual payment amount, which can significantly affect their penalty calculation.

Many filers also misuse the short method. The short method is only applicable under certain conditions, such as having made no estimated tax payments or having paid them in four equal amounts. If someone has made late payments or payments that were not equal, they should not use this method. Misusing it can result in a larger penalty than necessary, which is an avoidable mistake.

In addition, individuals sometimes forget to include all relevant income sources when calculating their estimated tax payments. This oversight can lead to an underreporting of income, which directly affects the penalty owed. It’s crucial to consider all sources of income, especially if they vary throughout the year.

Another area of confusion is related to the timing of payments. Some people fail to recognize that payments made early can affect the penalty calculation. If a payment is made before the due date, it may lead to discrepancies in the penalty amount if not handled correctly. Understanding how to report these payments accurately is essential.

Moreover, many filers neglect to complete all necessary lines of the form. For instance, skipping line 23, which indicates underpayment, can lead to incorrect calculations later in the form. Each line serves a purpose, and missing one can throw off the entire calculation.

Additionally, failing to account for the number of days after the due date of an installment can lead to miscalculations. The form requires individuals to track these days carefully, as they impact the penalty amount. Ignoring this detail can result in a higher penalty than anticipated.

Lastly, individuals often forget to attach the D 422 form to their tax return when required. If the underpayment is not reported, it can lead to penalties that could have been avoided. Ensuring that all necessary documentation is included with the tax return is vital for compliance.

By being aware of these common mistakes, individuals can navigate the D 422 North Carolina form more effectively. Taking the time to understand the requirements and double-checking calculations can save time, money, and stress in the long run.

North Carolina Department of Insurance Phone Number - The document should be printed clearly to ensure legibility for processing by authorities.

For individuals seeking to navigate legal processes, understanding the significance of a Notary Acknowledgement is crucial. This document, which verifies a signer's identity and their willingness to sign, can be efficiently tackled using the convenient Notary Acknowledgement form resources available online.

North Carolina Workers Compensation Laws - This request is based on North Carolina General Statute 50-13.1.

Nc Individual Income Tax - Date fields for both declarer and radiation safety officer are included.

The D 422 North Carolina form, which addresses the underpayment of estimated tax by individuals, shares similarities with Form 1040-ES, the Estimated Tax for Individuals form used federally. Both forms serve to calculate whether taxpayers owe a penalty for underpayment of estimated taxes. While Form 1040-ES is used for federal tax purposes, D 422 focuses specifically on North Carolina state taxes. Each form requires individuals to assess their tax liabilities and compare them against the estimated payments made throughout the year. Furthermore, both forms include methods to calculate penalties based on the timing and amount of payments made, ensuring that taxpayers can accurately determine their obligations.

In Texas, ensuring proper documentation during the transfer of pet ownership is essential, and the Puppy Bill of Sale offers a straightforward solution to clarify the terms of the exchange, providing both parties with peace of mind regarding the transaction.

Another document akin to the D 422 is Form D-422A, the Annualized Income Installment Worksheet. This form is designed for individuals whose income fluctuates during the year, allowing them to adjust their estimated tax payments accordingly. Similar to the D 422, Form D-422A helps taxpayers determine if they owe a penalty for underpayment, but it does so by allowing for a more nuanced calculation based on annualized income rather than a flat estimate. This flexibility can significantly impact the penalty amount, making it a crucial tool for those with variable income streams.

Form 2210, the Underpayment of Estimated Tax by Individuals, is another related document. Used for federal tax purposes, this form helps taxpayers calculate penalties for not paying enough estimated tax throughout the year. Like the D 422, Form 2210 includes methods to compute the penalty based on the amount and timing of payments. Both forms require similar information about tax liabilities and payments made, highlighting the commonality in addressing underpayment issues at both state and federal levels.

Form 4868, the Application for Automatic Extension of Time to File U.S. Individual Income Tax Return, also bears resemblance to the D 422. While its primary purpose is to extend the deadline for filing tax returns, it indirectly relates to the concept of estimated tax payments. Taxpayers who file Form 4868 must still consider their estimated tax payments and potential penalties for underpayment, as failing to pay enough can lead to penalties regardless of an extension to file. Both forms emphasize the importance of meeting tax obligations, even when deadlines are adjusted.

Form NC-40, the North Carolina Individual Estimated Income Tax Payment Voucher, serves a similar function as the D 422 in that it deals with estimated tax payments. While the D 422 assesses penalties for underpayment, NC-40 is used to make the actual estimated tax payments. Both documents require taxpayers to calculate their expected tax liability and ensure that they are making sufficient payments throughout the year to avoid penalties. This connection underscores the importance of proactive tax management in both forms.

Lastly, Form 1099, specifically the 1099-MISC or 1099-NEC, is relevant when discussing estimated tax payments. These forms report various types of income, such as freelance or contract work, which may not have tax withheld. Taxpayers receiving income reported on these forms must consider their estimated tax obligations and potential penalties for underpayment, similar to the considerations outlined in the D 422. Both documents highlight the necessity for individuals to actively manage their tax responsibilities, especially when income is not subject to withholding.

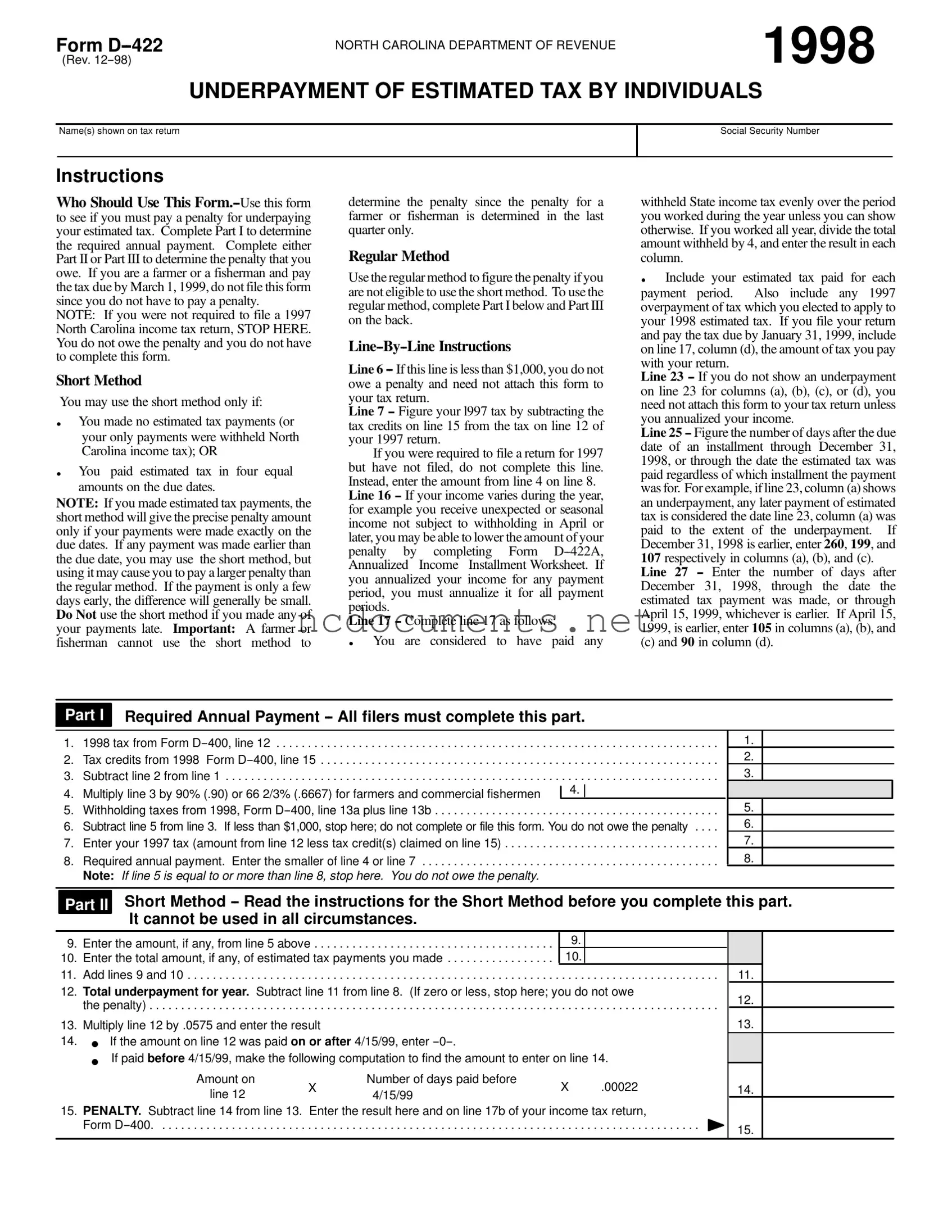

1. The D 422 form is used to determine if you owe a penalty for underpaying your estimated tax in North Carolina.

2. Complete Part I to calculate your required annual payment. You must then fill out either Part II (Short Method) or Part III (Regular Method) to find out the penalty amount.

3. If you are a farmer or fisherman and pay your tax by March 1, 1999, you do not need to file this form, as no penalty applies.

4. The Short Method is only applicable if you made no estimated tax payments or if you paid in four equal amounts on time. If any payment was late, use the Regular Method instead.

5. If your total required payment is less than $1,000, you do not owe a penalty and do not need to attach this form to your tax return.

6. For those with varying income throughout the year, consider using Form D-422A to potentially lower your penalty by annualizing your income.

7. Carefully follow the line-by-line instructions provided on the form to ensure accurate calculations and avoid unnecessary penalties.

The D 422 form is designed to help individuals determine whether they owe a penalty for underpaying their estimated tax. It guides users through calculating their required annual payment and assessing any penalties based on their tax situation. This form is particularly important for those who may have fluctuating income or who did not meet their estimated tax payment obligations throughout the year.

This form should be used by individuals who are unsure if they need to pay a penalty for underpaying their estimated taxes. If you did not have to file a 1997 North Carolina income tax return, you do not need to complete this form. Additionally, farmers or fishermen who pay their taxes by March 1, 1999, are exempt from filing this form, as they are not subject to penalties in this scenario.

There are two methods available for calculating the penalty: the Short Method and the Regular Method. The Short Method can be used if you made no estimated tax payments or if your payments were made in four equal amounts on the due dates. However, if you made any payments late, you should use the Regular Method instead. The Regular Method requires more detailed calculations and is necessary for those who do not qualify for the Short Method.

If your required annual payment is less than $1,000, you do not owe a penalty and do not need to attach the D 422 form to your tax return. This threshold is important, as it exempts many taxpayers from the complexities of penalty calculations.

Yes, if your income fluctuates throughout the year, you may be able to lower your penalty by using Form D-422A, the Annualized Income Installment Worksheet. This form allows you to annualize your income for each payment period, which can help accurately reflect your tax obligations and potentially reduce any penalties owed. However, if you choose to annualize your income for one payment period, you must do so for all periods.

Completing the D 422 form is essential for individuals who may face penalties for underpaying estimated taxes. This form allows taxpayers to assess their tax obligations accurately. Follow these steps to fill out the form correctly.

| Fact Name | Details |

|---|---|

| Purpose | This form helps individuals determine if they owe a penalty for underpaying their estimated tax. |

| Eligibility | Farmers and fishermen can skip this form if they pay their tax by March 1, 1999. |

| Methods | There are two methods to calculate the penalty: the Short Method and the Regular Method. |

| Exemptions | If your required annual payment is less than $1,000, you do not owe a penalty. |

| Governing Law | This form is governed by North Carolina General Statutes, specifically related to income tax regulations. |