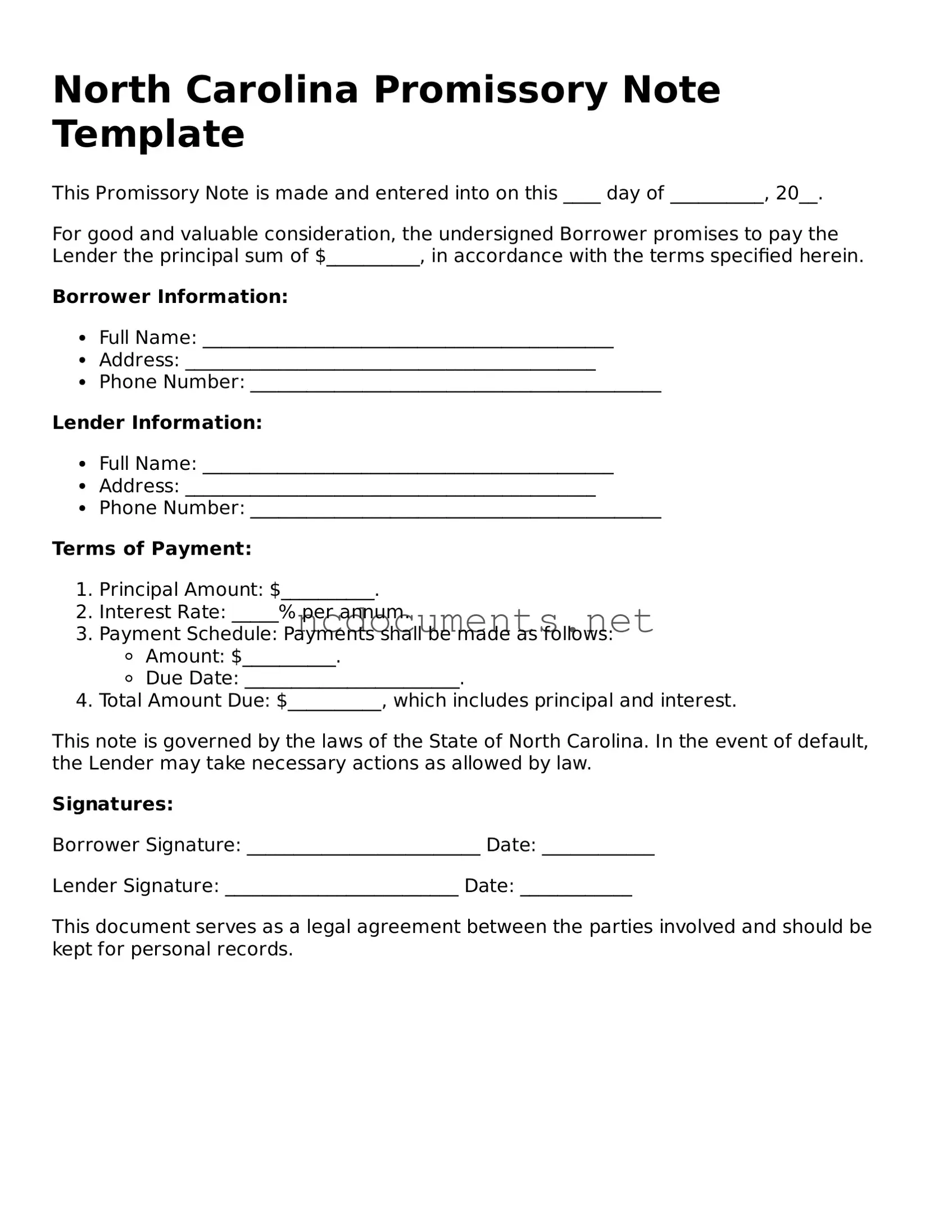

Blank North Carolina Promissory Note Template

Blank North Carolina Promissory Note Template

Filling out a Promissory Note in North Carolina can seem straightforward, but many people make common mistakes that can lead to complications down the line. Understanding these pitfalls can save you time and stress. Here are seven mistakes to avoid.

One frequent error is not including all necessary details. A Promissory Note must clearly state the amount borrowed, the interest rate, and the repayment schedule. Omitting any of these details can lead to confusion or disputes later. Always double-check that you’ve included everything required.

Another mistake is using vague language. It's crucial to be specific about terms and conditions. For example, instead of saying "repay in a few months," specify the exact date. Clear language helps both parties understand their obligations and reduces the likelihood of misunderstandings.

Many people also forget to sign the document. It might seem obvious, but without a signature, the note is not legally binding. Ensure that both the borrower and lender sign the document. It’s a simple step that can prevent significant issues later.

Another common oversight is not having a witness or notarization. While North Carolina doesn’t require a Promissory Note to be notarized, having a witness can add an extra layer of security. A witness can help verify the authenticity of the agreement if disputes arise.

People often fail to keep copies of the signed document. After everything is filled out and signed, make sure to keep a copy for your records. This document serves as proof of the agreement and can be essential if any issues come up in the future.

Additionally, not considering state laws can lead to problems. North Carolina has specific regulations regarding interest rates and repayment terms. Familiarize yourself with these laws to ensure that your Promissory Note complies and is enforceable.

Finally, many rush through the process and neglect to review the document thoroughly. Take your time to read through the entire note before finalizing it. Look for any errors or unclear terms. A little extra time spent reviewing can save a lot of headaches later on.

By being aware of these common mistakes, you can fill out your North Carolina Promissory Note with confidence. Taking the time to ensure accuracy and clarity will help protect both parties involved in the agreement.

How to Transfer Home Ownership - This form allows an individual to relinquish their claim to a property without guaranteeing the title.

North Carolina Separation Agreement Template - This document helps clarify responsibilities and rights after separation.

North Carolina Employee Handbook Requirements - Review the guidelines for expense reimbursements.

The North Carolina Promissory Note form shares similarities with a Loan Agreement. Both documents outline the terms of a loan between a borrower and a lender. They specify the principal amount, interest rate, repayment schedule, and consequences of default. While a promissory note is often simpler and focuses primarily on the borrower's promise to repay, a loan agreement may include additional clauses, such as covenants and representations, providing more comprehensive terms for the transaction.

A Secured Promissory Note is another document akin to the North Carolina Promissory Note. This version includes collateral to secure the loan, which provides the lender with a claim to the specified asset if the borrower defaults. Like the standard promissory note, it details the repayment terms, but the inclusion of collateral adds a layer of security for the lender, making it a more robust option for high-risk loans.

When purchasing an ATV in Colorado, it's crucial to have the correct documentation to ensure a seamless transfer of ownership. The Colorado ATV Bill of Sale form serves this purpose by providing a transparent record of the transaction. For more detailed information on how to obtain and fill out this essential document, you can visit All Colorado Documents, which offers a convenient resource for buyers and sellers alike.

An Installment Loan Agreement is also similar. This document outlines a loan that is repaid in regular installments over a set period. Both the Installment Loan Agreement and the North Carolina Promissory Note detail the amount borrowed and the payment schedule. However, the Installment Loan Agreement often includes more specifics about the payment process and any fees associated with late payments, making it more detailed than a standard promissory note.

A Personal Loan Agreement is comparable as well. It serves as a contract between individuals, detailing the terms of a personal loan. Similar to the North Carolina Promissory Note, it specifies the loan amount, interest rate, and repayment terms. However, a Personal Loan Agreement may also include conditions regarding the use of funds and requirements for borrower disclosures, which are not typically found in a standard promissory note.

The Mortgage Note is another document that bears resemblance to the North Carolina Promissory Note. This note is used in real estate transactions and serves as a written promise to repay a loan secured by real property. Both documents outline the borrower's commitment to repay, but the Mortgage Note is tied to a specific property and includes terms related to foreclosure and property rights, adding complexity to the agreement.

A Car Loan Agreement shares similarities with the North Carolina Promissory Note as well. This document outlines the terms of financing for a vehicle purchase. Like the promissory note, it specifies the amount financed, interest rate, and repayment terms. However, a Car Loan Agreement may also include additional details about the vehicle, warranties, and responsibilities of both parties, which are not typically included in a standard promissory note.

A Business Loan Agreement is also comparable. This document is used when a business borrows funds and includes terms similar to those found in the North Carolina Promissory Note. It outlines the loan amount, interest rate, and repayment schedule. However, it often includes specific conditions related to the business's operations and financial performance, which are generally absent from personal promissory notes.

The Student Loan Agreement is another document that aligns with the North Carolina Promissory Note. This agreement outlines the terms under which a student borrows money to pay for education expenses. Both documents specify the loan amount, interest rate, and repayment terms. However, the Student Loan Agreement often includes provisions related to deferment, grace periods, and forgiveness options, reflecting the unique nature of educational financing.

A Credit Card Agreement is also similar in nature. This document outlines the terms of borrowing through a credit card, including the credit limit, interest rates, and repayment obligations. While a credit card agreement functions differently than a promissory note, both documents require the borrower to repay borrowed funds under specified terms. The Credit Card Agreement typically includes more detailed information about fees and penalties, which are less common in a standard promissory note.

Lastly, a Lease Agreement can be compared to the North Carolina Promissory Note. While primarily used for renting property, a Lease Agreement may include a provision for a security deposit or advance rent, similar to the collateral aspect of a secured promissory note. Both documents establish a financial obligation, although the Lease Agreement focuses on the rental terms and conditions rather than a direct loan.

Filling out and utilizing the North Carolina Promissory Note form can seem daunting at first, but understanding its key components can simplify the process. Here are some important takeaways to consider:

A promissory note is a written promise to pay a specific amount of money to a designated person or entity at a defined future date or on demand. In North Carolina, this document serves as a legal instrument that outlines the terms of the loan, including the principal amount, interest rate, payment schedule, and any applicable fees. It is important for both lenders and borrowers to understand the terms outlined in the note to avoid disputes later on.

For a promissory note to be valid in North Carolina, it should include several key elements:

Yes, a properly executed promissory note is legally binding in North Carolina. This means that if either party fails to adhere to the terms, the other party has the right to seek legal recourse. It is crucial for both parties to understand their obligations under the note. Keeping a copy of the signed document is advisable for future reference and to support any claims if disputes arise.

Yes, modifications to a promissory note can be made after it has been signed. However, both parties must agree to the changes, and it is best practice to document any amendments in writing. This new document should be signed by both parties to ensure that the modifications are enforceable. Verbal agreements may not hold up in court, so written documentation is key.

If a borrower defaults on a promissory note, the lender has several options. Initially, communication with the borrower is essential. Sometimes, a simple discussion can lead to a resolution. If that does not work, the lender may consider the following steps:

It is important to approach these situations thoughtfully and to consider all options before proceeding with legal action.

After you have gathered the necessary information, you are ready to fill out the North Carolina Promissory Note form. This document requires specific details about the borrower, lender, and the terms of the loan. Follow these steps carefully to ensure accuracy.

Once completed, make copies for both the borrower and lender. Keep the original in a safe place for future reference.

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money at a specified time. |

| Governing Law | The North Carolina Uniform Commercial Code (UCC) governs promissory notes in North Carolina. |

| Parties Involved | The note involves two parties: the maker (borrower) and the payee (lender). |

| Essential Elements | A valid promissory note must include the amount, the interest rate, and the repayment terms. |

| Interest Rate | North Carolina law allows for both fixed and variable interest rates in promissory notes. |

| Enforceability | The note is enforceable in court if it meets all legal requirements and is signed by the maker. |

| Default Consequences | If the maker defaults, the payee may pursue legal action to recover the owed amount. |